By Seppo Ihalainen - CEO, Founder, Firma-Rise

AI is not a bubble. But parts of the AI real estate story may be.

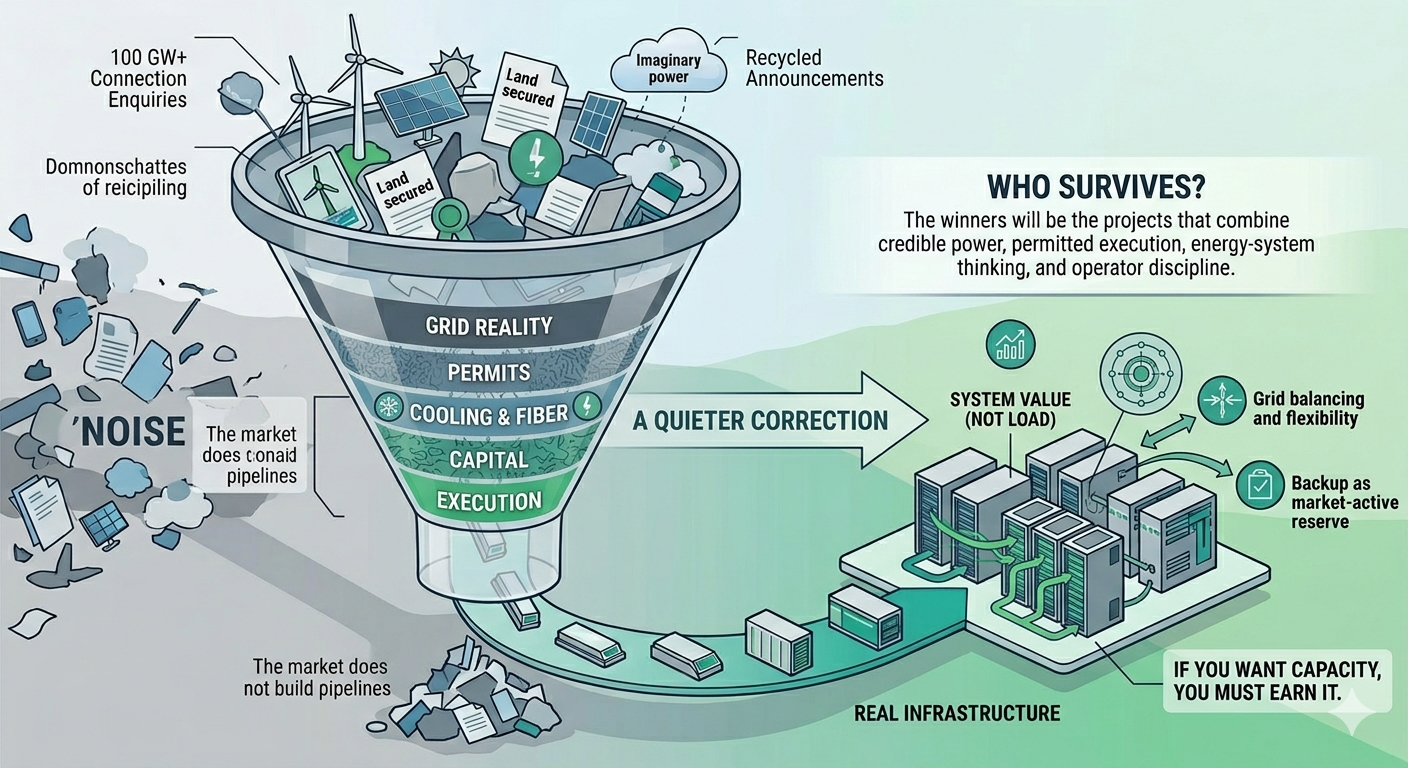

What worries me is not demand for compute. That is real. What worries me is the widening gap between what gets announced and what can actually be built. Land gets secured. Megawatts get marketed. “Power secured” gets repeated. Partnerships get announced. But delivery still has to survive the real filters: grid reality, permits, timing, cooling, fiber, capital, and execution. The market does not build pipelines. It builds what is real.

That is why I do not think the market necessarily ends with one dramatic crash. The correction may be quieter than that. It may simply happen project by project.

The bubble may not burst — it may get filtered

We have seen this pattern before in infrastructure. Big pipelines create big excitement, but only a fraction becomes reality.

That is why I keep using offshore wind as a reference point. In Finland, the announced pipeline is enormous, but the realistic build-out is much smaller. The lesson is simple: pipeline narratives are not deployment. Business logic filters ambition. Grid reality filters promises. Capital filters weak projects. Execution filters the rest.

The question is whether AI data center real estate is now entering the same phase.

The market also has a short memory. High-expectation projects are not new. Nordic and European markets have already seen years of bold data center narratives, quiet delays, recycled announcements, and capacity that never arrives. Berlin is only the latest reminder. It is a strong market with real demand, but even there the gap between planned capacity and actual delivery has raised doubts about how much of the announced pipeline will really be built.

That does not mean the market is fake. It means the market needs more discipline.

The biggest risk is imaginary power

One of the loosest phrases in the sector may be: “power secured.”

Too often that phrase hides more than it reveals. It may mean an inquiry, a conditional path, non-firm capacity, or a timeline that ignores reinforcement, maturity criteria, or permitting reality. That is why I keep coming back to the phrase imaginary power. The biggest risk in AI infrastructure is not chips. It is the assumption that electricity, permits, and delivery will somehow line up because a slide says they will.

Finland’s own policy and grid discussion is moving in the same direction.

The national roadmap notes that large data center projects take years, ramp up gradually, and sit inside a much wider power-system transition. It also records Fingrid’s earlier estimate of roughly 70 GW of grid connection enquiries, nearly half linked to data centers at that point.

But the more important update now comes directly from Fingrid’s latest public communication: cumulative consumption-side connection enquiries have already risen to over 100 GW, and more than half relate to data center projects. In other words, the market is already even larger on paper than it looked just a few months ago.

And Fingrid’s public action plan is also conceptually important. It argues that locating production and consumption closer to each other enables faster connections and a more cost-efficient grid; it calls for open and transparent capacity allocation practices in congestion situations; and it says flexible transmission-grid connections should be developed so that more projects can be connected faster. That is not the language of unlimited passive demand. It is the language of prioritisation, flexibility and system fit.

Owning assets is not the same as building a platform

Another confusion in the market is the belief that collecting ingredients makes you a credible data center developer.

Land. Grid rights. Wind. Solar. BESS. A recognizable advisor. A headline partnership.

Those may all help. But they are not the same as having a real platform.

There are three levels of credibility: the asset story, the energy system story, and the real DC platform. The first is easy to announce. The second is more credible, but still incomplete. The third is what customers and investors should actually test: mission-critical design know-how, the ability to design, build and operate, real digital infrastructure understanding, delivery discipline, and uptime culture. Borrowed credibility is not the same as built capability.

This is not only a Finnish issue

The same physical reality is now visible in the U.S. as well. Bloomberg recently reported that more than half of the U.S. data centers planned for this year are expected to be delayed because the electrical equipment needed to bring them online is hard to obtain. A related Bloomberg feature points to shortages in transformers, switchgear and batteries, even as the largest tech companies are committing over $650 billion to AI infrastructure. Money is not the only constraint anymore. Physical infrastructure is.

That is why the real bottleneck is no longer just semiconductors. It is the full chain of power, equipment, grid access and delivery capability.

The real divide is contribution versus consumption

This is where the conversation gets more interesting.

The market should stop asking only whether a project is “good” or “bad” real estate. A better question is whether it creates system value or merely adds system load.

That is also where Finland’s policy discussion becomes important. Its National Roadmap for Data Centres does not just promote more data centers. It starts to define what a high-value data center actually is. According to the report, a high-value data center typically creates economic value, registers with a designated authority, and actively contributes to organising power generation and improving grid functioning in order to increase flexibility during periods of peak electricity prices. Finland also says it will give priority to data centers that support the functioning of the power system, participate in balancing, use energy and water efficiently, and recover waste heat where possible.

That is a meaningful shift.

It means the conversation is moving beyond passive consumption. Not every megawatt should automatically qualify for the same incentives, the same public trust, or the same political support. High value should mean high responsibility. That logic is already visible in the roadmap’s proposed measures: electricity tax relief for high-value data centers, a fossil-free flexibility scheme, and a registration requirement.

Beyond incentives

This is why the next step should be more ambitious than another generic subsidy.

If Finland is serious about high-value data centers, then the idea should be productised more clearly. One possible direction would be a hybrid flex connection: one connection model combining load, generation, and storage, with connection terms that require flexibility and grid support; a model where backup becomes market-active reserve rather than idle insurance; and a model where incentives are linked to measurable contribution.

It creates a framework that encourages developers to adapt their design and business models, rather than relying on legacy approaches that enable capacity without requiring system contribution. While similar solutions can already be implemented under existing connection models, they remain optional. A defined hybrid model would make this behaviour expected — and, if linked to broader incentives, economically meaningful.

Put simply - If you want capacity, you must earn it.

Whether Finland adopts that exact model is secondary. The bigger point is that passive consumption will become harder to justify.

And that is healthy.

Because some data centers are infrastructure. Others are just electricity sinks.

That distinction is no longer rhetorical. It is becoming a policy question, a grid question, and soon a market question.

Who survives?

I do not think AI demand disappears.

I do think the market becomes harsher.

Harsher on imaginary power. Harsher on site marketing without execution. Harsher on asset collection without platform capability. Harsher on projects that want incentives without contribution.

So when the market starts filtering, who survives?

Not the loudest. Not the biggest on paper. Not the best at storytelling.

The winners will be the projects that combine credible power, permitted execution, energy-system thinking, and operator discipline. In other words: not just AI real estate, but real infrastructure.